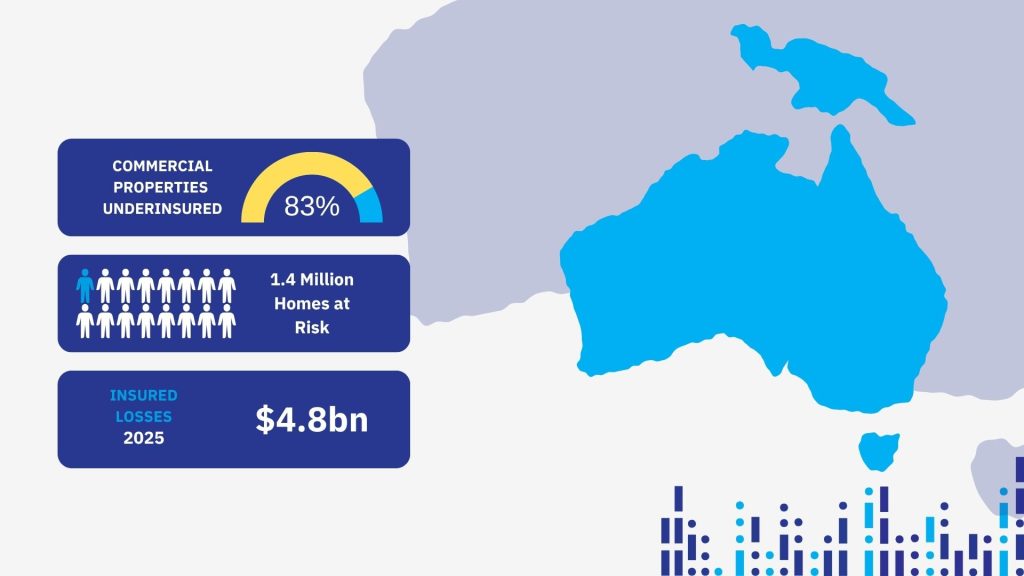

The Australian property insurance landscape in 2026 is defined by extreme climate volatility, sweeping legislative reforms, and escalating macroeconomic pressures. Extreme weather events generated an estimated $4.8 billion in insured losses across 2025, driving commercial and retail premiums to historic highs.

Rising inflation and the technical demands of the National Construction Code (NCC) 2025, have revealed weaknesses in property valuation. Many property owners, pressured by living costs, often underinsure their properties by millions. To address this, industry professionals depend on quantity surveyors to accurately assess Value at Risk (VAR) and ensure adequate insurance coverage.

The Underinsurance Epidemic

Over the past three years, cumulative inflation has pushed up the overall cost of living by approximately 13.6%. When household budgets and corporate cash flows are squeezed, insurance is often viewed as a flexible expense rather than a non-negotiable safeguard.

Research from The Australia Institute reveals that approximately 20% of households admit their primary residence is uninsured or underinsured, placing 1.4 million homes at acute risk. If a middle-wealth household’s uninsured home is destroyed in a natural disaster, they stand to lose 74.3% of their total wealth. In the commercial sector, the situation is equally dire, with up to 83% of property owners underinsured.

Brokers acutely understand how to manage costs and risks for their clients in this inflationary environment. To compensate for high premiums, brokers often help clients reduce upfront costs by increasing the policy excess. While this is a great strategy to manage cash flow, it will cost the client in the long run if the property is underinsured. The sum insured on a commercial property policy is fundamentally more important than just increasing the excess; if the sum insured is correct, the policyholder gets the maximum return on the policy when the excess is increased, ensuring long-term survival rather than an unbridgeable out-of-pocket shortfall.

Highlight that up to 83% of commercial properties are underinsured and 1.4 million homes are at acute risk. Include the statistic that extreme weather events generated $4.8 billion in insured losses across 2025.

Supply Chain Volatility: “Where Are the Materials Coming From?”

A frequent misconception occurs when a client looks at a commercial asset and declares, “It is a 5 million dollar building.” However, a property cannot simply be replicated by transferring $5 million. The critical question must be asked: Where are the materials coming from?

Global supply chains remain fractured, meaning the procurement of structural timber, steel, and specialised glass involves extended delays and inflated building material costs. These logistical bottlenecks introduce a hidden excess: the cost of time. Supply chain delays directly extend reconstruction timelines, placing immense strain on Business Interruption (BI) policies. If the sum insured does not account for a protracted 24-to-36-month rebuild, BI limits will exhaust prematurely, forcing the business to fund its own survival out of pocket.

The Myth of “Like for Like” and the NCC 2025

When a property is destroyed, it cannot be replaced “like for like.” In the modern regulatory environment, it must invariably be brought up to code. The NCC 2025, rolling out from May 2026, introduces a sweeping suite of technical upgrades that drastically elevate the cost of rebuilding.

Key NCC 2025 mandates include:

- Condensation Management: Direct-fix cladding is banned in colder climate zones, requiring builders to utilise complex wall cavities and specializsd vapour permeable sarking.

- Commercial Energy Efficiency: Strict new restrictions on HVAC systems, mandatory on-site solar photovoltaics, and artificial lighting demand controls require the integration of high-tier capital equipment.

- Carpark Fire Safety: Enhanced structural and suppression requirements have been introduced to address the extreme temperatures of modern vehicle fires.

The cost implications are exacerbated by a highly fragmented state-by-state adoption process. In New South Wales alone, state-specific variations have ballooned to more than 210 in the 2025 edition, adding layers of bespoke local regulation. Without an “Increased Cost of Compliance” allowance specifically calculated into the sum insured, policyholders are left to fund these mandatory upgrades themselves.

Commercial Blind Spots: Concrete and Carparks

One of the most persistent errors in commercial property insurance is ignoring the foundational infrastructure. People routinely forget about the concrete.

An Insured might look at their 7.700sqm Industrial Shed with an 1,100 square meter mezzanine and assume a minimal sum insured of $5m is sufficient, as they only need to insure the above-ground warehouse structure. However, if a severe commercial fire sweeps through the building, what happens if the integrity of the concrete footprint is compromised.

Extreme thermal exposure (temperatures exceeding 300°C) causes the cement paste to undergo structural calcination, irreversibly losing its binding properties. Forensic engineers specifically look for pink discoloration, spalling, and anchorage failure to identify this thermal degradation. When evaluated correctly by a quantity surveyor accounting for the demolition, forensic testing, and total re-pouring of the compromised concrete and carparks, the true insurance replacement value of the risk would be estimated at a staggering $16 million.

Agricultural Vulnerabilities: The Valuation Trap

Agribusinesses oversee extensive assets such as fences, irrigation pumps, sheds, and large equipment. Amid unpredictable climate conditions, the most vital aspect of farm insurance is the method used for valuing these assets:

| Valuation Method | Definition | Key Risk for the Policyholder |

| Indemnity Value (ACV) | Replacement cost minus depreciation for age, wear, and tear. | Massive out-of-pocket shortfalls. For example, a 64-year-old shed or a 15-year-old fence yields a minimal payout due to heavy depreciation deductions. |

| Replacement Cost | Cost to replace the asset with a new one of similar quality. | The Co-Insurance (Average) Clause penalises partial claims if the total sum insured is inaccurate. |

Insuring assets like fencing or pumps on an indemnity basis can leave farmers unable to replace them due to rapid depreciation and rising costs. Replacement Cost insurance needs precise valuations; if a packing shed is underinsured by 50%, co-insurance means only half of any damage claim will be paid.

The Indispensable Role of the Quantity Surveyor

To successfully navigate this landscape, property owners and brokers must utilise accurate evaluation tools and professional expertise. While the Insurance Council building calculator can provide an initial, approximate guide to help property owners estimate replacement costs and avoid pure guesswork, the ICA explicitly notes that these tools do not replace professional advice and take no responsibility for the final costs.

Therefore, for accurate commercial valuations, property owners must abandon generic online calculators and utilise the forensic expertise of a certified quantity surveyor. While desktop “evaluation requests” are useful for tracking broad inflationary trends or assessing remote rural properties, they cannot accurately capture complex commercial assets.

Ensuring accuracy requires a comprehensive site investigation. A specialised QS will physically walk the site, assessing the property “from the ground up” to capture the “whole property” scope, including retaining walls, intricate drainage, and the true extent of the concrete carparks.

Morse Building Consultancy offers precise evaluations that take into account demolition, professional fees, statutory charges, and anticipated replacement costs. They also provide calculated Indemnity Valuation Reports (IVR) and expert witness testimony to resolve complex claim disputes.

In today’s climate of heightened volatility, accuracy serves as a key protection. Engaging the expertise of a quantity surveyor provides a reliable method for establishing an appropriate and secure sum insured.