When an insurance claim is straightforward, a broker rarely has to dive into the granular details of a technical structural building report. But when brickwork cracks after a severe storm, a retaining wall unexpectedly shifts, or a roofline sags, the entire conversation changes.

The insured naturally believes the damage is fresh and event-related. The insurer, however, may spot signs of age, deferred maintenance, or historic movement. Suddenly, the broker isn’t just facilitating a claim, they could be translating complex evidence. A clear, independent structural report prepared by experienced building consultants or independent engineers acts as the circuit breaker that reduces confusion and moves a difficult file forward.

When it comes to interpreting structural building reports for insurance brokers, understanding the nuances is key to supporting clients and negotiating effectively with underwriters.

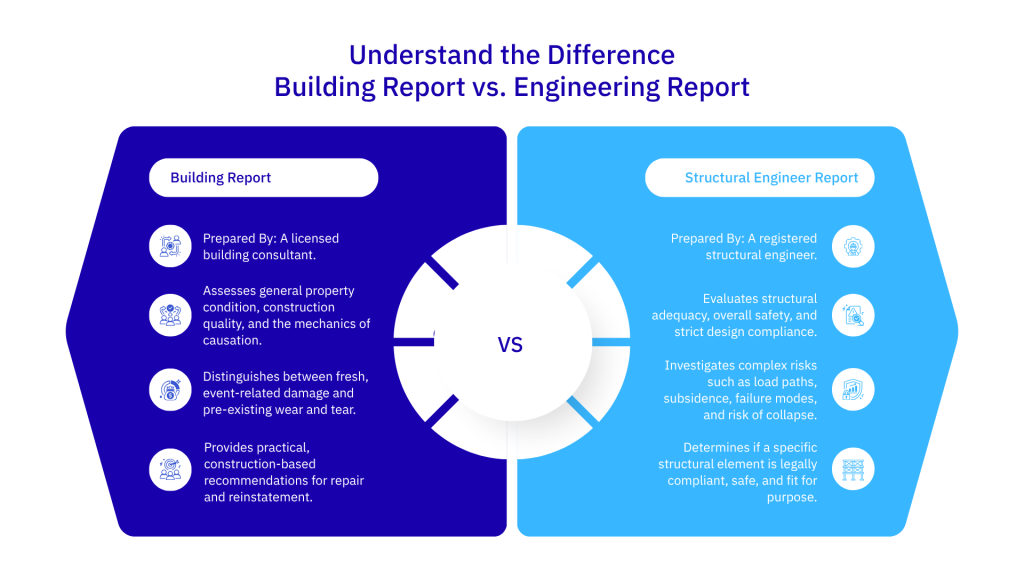

Understand the Difference Between a Building Report and a Structural Engineer Report

Not every technical report carries the same weight, nor do they answer the same questions. Treating them as interchangeable is a common pitfall.

Typically prepared by a licensed building consultant. These focus on the property’s condition, the cause of the damage, and the practical rectification process from a construction perspective. They detail whether damage appears event-related or pre-existing. While a tradie might be well-placed to discuss a practical repair method, an independent building consultant objectively assesses the defects, construction quality, and reinstatement requirements.

Conducted by a registered engineer. These are required when the core questions revolve around structural adequacy, safety, design compliance, load paths, and failure modes. If there is a risk of collapse, subsidence, or severe impact damage, an engineering report is essential.

This independent expertise is utilised when insurers need specialist advice regarding the cause of damage or the extent of necessary repairs. A registered structural engineer is usually necessary to determine if a structural element is safe, compliant, or fit for purpose.

Understanding when to use a structural engineer vs. a building consultant for insurance claims is the first step in ensuring the file progresses smoothly.

Read the Scope Before the Conclusion

The most critical page of a structural report isn’t always the final conclusion. It’s the instructions and scope.

Brokers should consider:

- What was the expert actually instructed to inspect?

- Was the brief limited to a single retaining wall or a specific storm event?

- Was invasive investigation explicitly excluded?

A narrow scope isn’t inherently a weakness, provided it is clearly defined. It only becomes a liability when a limited report is used to make broad, sweeping assumptions.

Causation is the Core of the Claim

In property claims, the damage list is secondary to causation.

A cracked wall simply proves an event occurred. The causation explains why it occurred. Was it a storm, an escape of liquid, footing movement, or simply a lack of maintenance?

Proving proximate cause in structural building damage reports is ultimately about answering whether a specific event triggered the loss under the policy terms, aligning with industry standards and AFCA recommendations.

Brokers should pay close attention to linking phrases like “consistent with,” “pre-existing,” or “progressive”. A robust report doesn’t just state an opinion, it builds a chain of reasoning supported by rainfall data, moisture readings, and site fall.

Verify Qualifications, Independence, and Evidence

The weight of a report relies heavily on the building consultant’s credentials and their independence. It is important to highlight that engineer registration rules vary significantly by state. Some states mandate that any professional engineering service provided in that state must be executed by a Registered Professional Engineer. A report accepted in one jurisdiction might not meet the statutory requirements of another, which is vital for brokers managing national portfolios.

Remember, evidence beats adjectives. A strong structural building report outlines the inspection date, site limitations, crack widths, moisture readings, and roof space observations. A robust report builds a chain of reasoning; supported by rainfall data, moisture readings, and site fall, that clearly distinguishes event-related damage vs. pre-existing defects in structural reports. This is the evidence trail brokers need before standing before an underwriter or claims adjuster.

The Importance of Compliance References

When a report cites the National Construction Code (NCC) or Australian Standards, take note. These references directly impact repair costs, engineer sign-offs, and underwriter appetite. The Australian Building Codes Board’s Evidence of Suitability handbook dictates that documentary evidence must support whether a design or material meets NCC requirements. A recommendation tied to a recognised standard is always stronger.

Translating Technical Language

Experts use cautious language to avoid overstating their findings beyond the available evidence.

Here is how to decode common phrases:

| Expert Phrase | What it Actually Means |

| “No structural distress was observed” | No visible failure was found during the inspection. It does not mean the building is entirely free of defects. |

| “Consistent with long-term deterioration” | The condition developed gradually over time, rather than from one sudden, insured event. |

| “Further investigation is required” | The current visual evidence isn’t enough for a final opinion. This may necessitate invasive inspections, monitoring, or geotechnical advice. |

| “Repairs should be designed by a structural engineer” | The issue is beyond a simple trade repair. It requires formal engineering design, a detailed scope, and certification. |

How Brokers Should Use a Structural Building Report

When communicating with clients, keep it simple. Explain what was inspected, what the expert found, the likely cause, and the next steps.

Never tell a client the report “accepts” or “declines” the claim. Because simply, a structural building report is expert evidence. The insurer makes the final coverage decision about a claim.

With underwriters, the report facilitates a clearer conversation about risks, active movement, non-compliant construction, or required remedial works. This evidence-based communication aligns with ASIC’s view of claims handling as a regulated financial service and meets the NIBA Insurance Brokers Code of Practice standards for honesty, integrity, and prioritizing client interests.

It is important to note. Never hesitate to seek clarification if a report lacks photographs, relies on unsupported conclusions, or features recommendations that don’t match the observed damage.

Consider this: “Can the expert clarify which evidence supports the causation finding, and whether the opinion is final or conditional?” This protects the client, assists the insurer, and keeps the discussion anchored entirely in facts.

A structural building report is not just a technical file note

It is a critical decision tool. By reading the scope, checking the building consultant or registered engineer’s credentials, isolating causation, and noting compliance issues, brokers can translate technical recommendations into practical steps.

When written by the right independent expertise, it provides brokers and their clients with exactly what they need in a complex property claim. A clear, defensible explanation they can confidently stand behind.