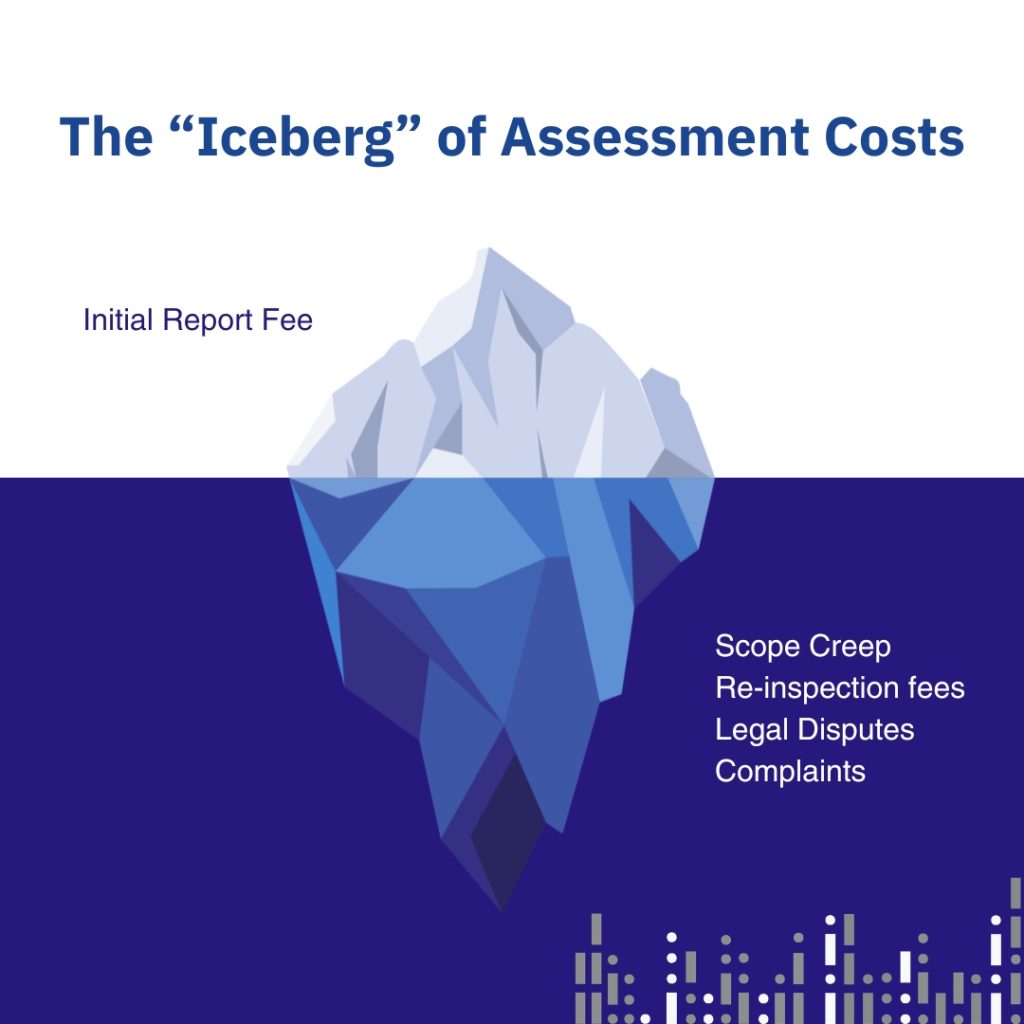

In the current insurance landscape, the pressure to reduce claim costs is relentless. We hear it in every meeting with insurers and claim managers: “Keep the costs down.” It is a directive that comes straight from the top, driven by shareholders and boards looking at the bottom line.

It is understandable. When claim volumes spike after a catastrophe, every dollar spent on assessment fees is scrutinized. However, there is a distinct difference between price and value. In our experience, the “cheapest” report often becomes the most expensive line item on a file because of the disputes, delays, and administrative heavy lifting it generates.

At Morse Building Consultancy, we often encounter the objection that a comprehensive, insurer-grade report might cost 30% more than a standard check-box inspection. But when you peel back the layers of a complex construction dispute, you almost always find that the root cause was an initial report that missed the detail.

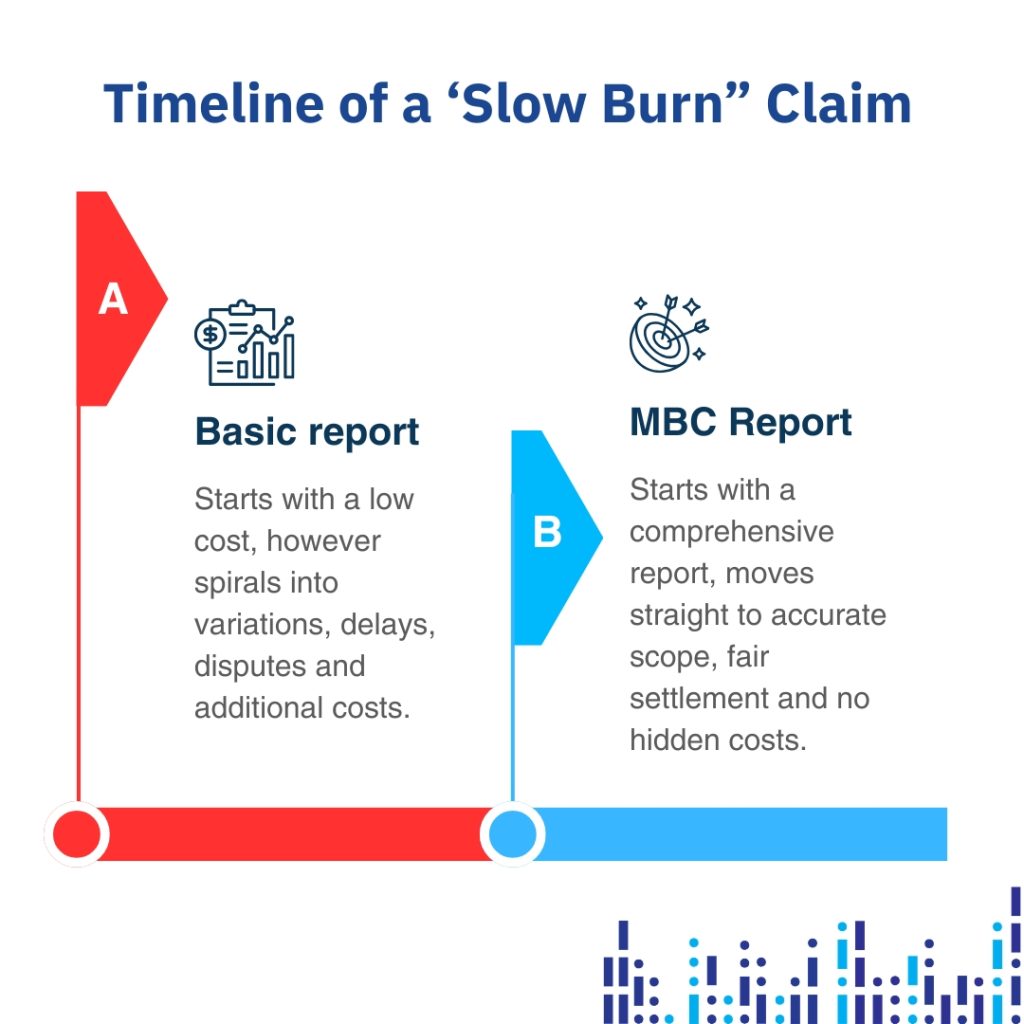

The “Slow Burn” Claim: A Case Study in False Economy

To understand the true cost of a “cheap” report, we have to look at the lifecycle of a claim.

Consider a recent example involving a residential flood claim. In this instance, a basic assessment was done early on. The initial report was brief, inexpensive, and quick. It estimated the damage at around $200,000, framing it as a repairable job. On paper, the insurer looked like they had a manageable claim.

Fast forward twelve months. The claim was still open. The policyholder was furious. The builder could not deliver the scope for the price, and variations were flying back and forth. The file had become toxic.

When we were eventually brought in to review the matter, it required a forensic deconstruction of the entire history. It took 275 hours of work, the engagement of an independent engineer, and meetings with builders on-site to finally get to the truth. The reality? It was a total loss from day one. The correct settlement was $800,000, not $200,000.

If a comprehensive builders report for insurance claim had been commissioned in the first week, the total loss would have been identified immediately. The claim could have been settled in a month. Instead, the insurer paid for a year of administrative churn, temporary accommodation, and reputational damage. The “cheap” initial report cost them exponentially more than a proper assessment ever would have.

Why “Scope” is the Secret to Dispute Resolution

Construction dispute resolution rarely happens in a courtroom. It happens on site, in the details of the Scope of Works (SOW). Disputes arise when there is ambiguity. If a report says “repair wall” but does not specify the method, the materials, or the extent of the strip-out, you are inviting conflict between the builder, the owner, and the adjuster.

A defensible building report can separate event-related damage from pre-existing issues and identifies all risks upfront. It must be granular. It is not enough to identify that a bathroom is damaged; we must determine if the waterproofing failure was sudden or if it was a long-term leak that pre-dated the event. This is where commissioning detailed structural damage reports becomes critical for adjusters who need to set accurate reserves.

This is where the “human element” of our work comes in. We know that behind every claim is a stressed property owner and an overworked claims consultant. When we provide a report that is vague, we are just passing the stress down the line. When we provide a report that is evidence-based and definitive, we give everyone the confidence to make a decision.

The Role of NCC Compliance in Ending Arguments

Another major driver of disputes is the gap between “like for like” repairs and lawful compliance. The National Construction Code (NCC) is not a suggestion; it is the law.

Disputes often turn on whether work meets the NCC. A common argument occurs when a builder wants to patch a roof, but the code requires a full upgrade of tie-downs or flashings to meet current wind ratings. If the initial assessment ignores this, the claim hits a wall when the certifier refuses to sign off.

Our approach is to anchor every recommendation in the code. We reference Deemed-to-Satisfy provisions and Performance Requirements directly in the report. This moves the conversation from “opinion” to “fact.” It is hard to dispute a scope when it is backed by a specific clause in the Australian Standards. This level of technical detail is what defines an independent building consultant. It creates a report that stands up to internal review, reinsurers, and, if needed, a tribunal.

For complex files, this often requires the input of registered engineers who can certify that the proposed rectification is not just a patch, but a compliant solution.

Investing in Clarity

We know that budgets are tight. But we also know that the most effective dispute resolution strategy is getting the scope right the first time.

When insurers engage Morse Building Consultancy, they are accessing a team that includes licensed building consultants and registered engineers who work together to produce a single, coordinated outcome. We do not just tick boxes. We investigate causation, we map moisture, and we quantify the work required to get the property back to a compliant state.

The premium for a detailed report is an insurance policy against the cost of a claim that could potentially drag on for years. Whether it is distinguishing storm damage from wear and tear or identifying a structural failure that others missed, clarity is the only currency that matters.

By investing in accurate damage reporting and forensic assessments upfront, insurers can close files faster, keep customers happier, and avoid the “slow burn” disasters that drain resources and morale.

Ready to close your complex files faster?

Stop the scope creep before it starts. Contact Morse Building Consultancy today to discuss how our forensic assessments can streamline your dispute resolution process.