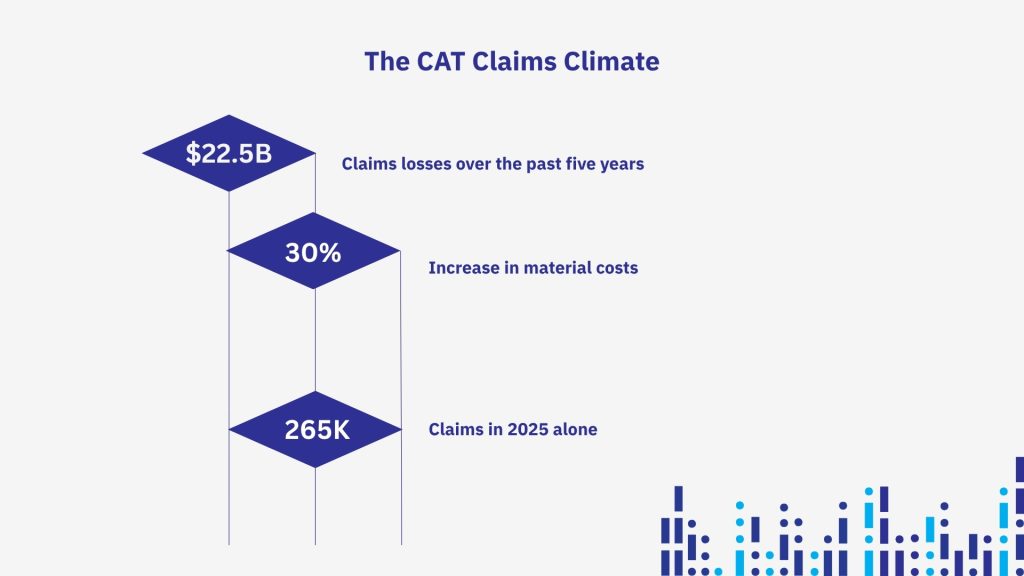

When a major weather event hits, the pressure to move fast is real. Quotes are needed, repairs feel urgent, and everyone wants clarity. But that urgency can create a problem of its own when the first repair estimate becomes the working truth. According to the Insurance Council of Australia’s 2025 industry fact pack, insured extreme weather losses have totalled $22.5 billion over the past five years, building material costs are on average 30 per cent higher than they were three years ago, and insurers have received almost 500,000 extreme weather claims from South East Queensland and northern New South Wales since 2022. The ICA’s 2026 update on 2025 losses adds that extreme weather cost almost $3.5 billion from 264,000 claims in 2025 alone.

The weather backdrop is not exactly calming either. The Bureau of Meteorology’s Annual Climate Statement 2025 recorded Australia’s fourth-warmest year on record, with national rainfall 8 per cent above the 1961 to 1990 average and wetter conditions across much of Queensland, coastal New South Wales and parts of the north. At the same time, the 2025 Occupation Shortage List shows that nearly half of trade roles are still in shortage, particularly in construction. This means, claims are landing in a repair market where weather pressure remains high and skilled labour is still hard to secure. That is exactly the sort of environment where broad assumptions become expensive.

What is an independent assessment after a catastrophe?

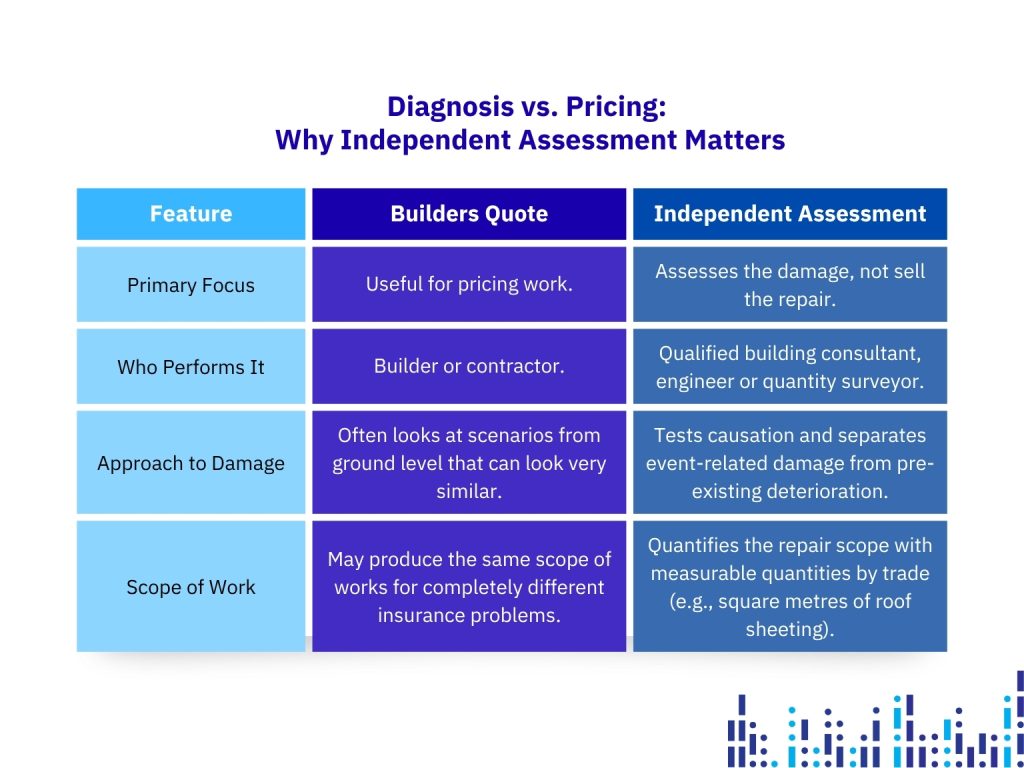

An independent assessment after a catastrophe is a site-based evaluation carried out by a qualified building consultant, engineer or quantity surveyor whose job is to assess the damage, not sell the repair. That distinction matters. A builder’s quote is useful for pricing work, but it does not always answer the more difficult questions sitting underneath a catastrophe claim. What damage was actually caused by the insured event? What was already there? What work is necessary to return the property to its pre-loss condition? Are there compliance issues that may affect the repair path once the building is opened up? A proper independent assessment is there to answer those questions with evidence.

That also means an independent assessment should do far more than confirm that damage exists. It should test causation, separate event-related damage from pre-existing deterioration, and quantify the repair scope in a way that can be explained to insurers, adjusters, owners and contractors alike. The General Insurance Code Governance Committee’s thematic inquiry raised concerns about expert reports that did not clearly demonstrate the link between the cause of damage and the loss. ASIC also found insurers did not have a systemic approach to overseeing the quality of independent expert reports. That is not a small technical issue. It goes to the heart of whether a claim decision is sound.

Why builder quotes alone are not enough after a catastrophe

Builders are essential to recovery, but diagnosis and pricing are not the same task. After a storm, a leaking roof may be the result of hail impact, wind-driven rain, box gutter overflow, failed flashings, corrosion, aged sealants, poor detailing or long-term maintenance issues that were merely exposed by the event. From ground level, some of those scenarios can look very similar. They are not the same insurance problem, and they should not produce the same scope of works. When a file moves forward on assumption rather than proof, that is when claim leakage starts to creep in.

Poor early evidence tends to echo all the way through the life of a claim. The Australian Financial Complaints Authority’s 2024-25 review of general insurance complaints shows 34,231 general insurance complaints were received that year, with delay in claim handling remaining one of the top issues and the average time to close a general insurance complaint at 96 days. The CGC also reported that in 2021-22 about 11,000 denied home insurance claims resulted in complaints. Better evidence at the start will not eliminate every dispute, but it does give claims teams a much stronger basis for decisions that can be explained and defended.

What a strong independent catastrophe assessment looks like on site

A good assessment starts with safety. After that, it gets practical very quickly. Inspectors should be looking beyond surface symptoms and into the details that actually change outcomes: damage patterns, ingress paths, fixings, flashings, drainage points, moisture spread, ceiling cavities, structural movement, and signs of older deterioration that may already have been present. They should compare what is observed on site with the timing and nature of the weather event, then explain the findings in plain English. Was the damage caused by impact, uplift, overflow or long-term failure? What is event-related, what is not, and why? That is the level of clarity catastrophe claims need.

Then comes quantification. A useful report should not stop at phrases like “roof damage throughout” or “water damage to multiple areas”. It should identify measurable repair quantities by trade, such as square metres of roof sheeting, linear metres of flashing, wet insulation, affected ceilings, strip-out requirements, temporary protection, access needs and specialist engineering input. That kind of reporting gives insurers cleaner reserving, gives adjusters a defensible scope, and gives builders a brief they can actually price properly. It also makes tender comparisons far more meaningful because everyone is pricing the same defined work.

Compliance needs to be checked early as well. The Australian Building Codes Board notes that the amended Premises Standards took effect on 29 July 2025, and NCC 2022 Amendment 2 was published the same day, including updated reference to AS 1428.1:2021. That particular amendment is about accessibility, but the broader lesson is relevant to catastrophe work more generally: code settings do move, and compliance questions should be considered before a scope is locked in, not halfway through the repair when time, cost and liability are already under pressure.

Why independent assessment leads to fairer outcomes

An independent assessment is not about cutting a legitimate claim. It is about clarifying it. Sometimes the investigation shows the true repair is smaller than first thought because the damage is localised and the broader quote swept in unrelated deterioration. Sometimes it shows the opposite, where concealed water damage, structural movement or secondary impacts mean the loss has been underestimated. Either way, the aim is the same: separate fact from assumption and create a repair scope that stands up later.

That is why independence matters so much after a catastrophe. In a market shaped by higher weather losses, warmer conditions, tight trade capacity and continued scrutiny of claims handling, factual assessment is not a luxury. It is a control measure. For insurers, loss adjusters, strata managers and property owners, an independent assessment after a catastrophe is often the clearest way to understand what actually happened, what needs to be repaired, and what can confidently be left out. Done well, it supports fairer outcomes, tighter scopes and fewer avoidable disputes.

When the facts matter, independent expertise makes the difference

Our team of consultants, engineers and quantity surveyors provides clear, evidence-based assessments that help define damage, quantify repair scope and support fairer, more efficient claim outcomes.

For immediate support contact the MBC team today.